Take my money and lie to me... again (now with NEW shenanigans!)

This will be the third time I’ve written specifically about private assets under the “take my money and lie to me” title, and honestly, I wish I didn’t have to do it.

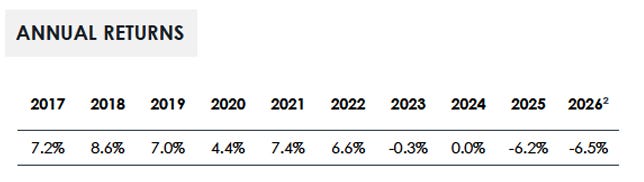

The first time I did so, in December of 2022, a large Canadian mortgage lender with a sterling reputation decided that they would suspend redemptions on a fund that was marketed to investors as a safe, high-yielding fixed income alternative. As I write this in early 2026, the fund still has not resumed business as usual.

The investment returns, once reliably in the high single digits, since turned negative.

Oops!

But this was just the first of many. There are others. I have a client who owns one of these failing private funds from their prior advisor. We are trying to help them sell this thing, to no avail. Last quarter the fund manager was able to redeem 0.07% of the requested units for sale. That’s not a typo. That’s seven one-hundredths of one percent.

In other words, the client is effectively trapped.

And then this week news hit that yet another private Canadian real estate investment fund would be freezing redemptions, and is considering going public to grant their unitholders liquidity. This seems to be to be a fascinating opportunity to see what kind of value the public markets are willing to place on non-traded assets. I’m not sure exactly how this story ends, but it could accelerate the rush out of private funds.

(In case you’re wondering, I’m purposely leaving out the names of these firms to avoid dealing with the inevitable blowback from advisors who have client money in these funds. Let’s just say, if you know, you know. And you probably wish you didn’t.)

Look, there’s a clear pattern emerging here, and it’s not limited to the Canadian real estate market. South of the border, things are not going too great either. Blue Owl Capital (Redefining alternatives®) can’t seem to get its name out of the news.

But don’t forget about BlackRock, which limited redemptions in a flagship private credit fund for the first time ever.

Or Blackstone, which reportedly had to inject $400 million of its own capital into a fund to meet redemption requests.

Or this private German pension fund for dentists that blew up €1.1 billion speculating in private assets (oops!)

Meanwhile, this week the FT published a piece explaining how two private equity firms are offering UBS Wealth Management a cut of their performance fees in exchange for pushing their private capital products to their client base, made up of some of the world’s wealthiest private client investors. This isn’t unique, and it tells you a lot about whose interests your high end “wealth manager” is serving when he or she loads your portfolio up with these funds. While the current investors are clamoring to get out, your “trusted advisor” is using your wealth to provide exit liquidity.

Tone deaf marketing (aka making stuff up and hoping they don’t notice)

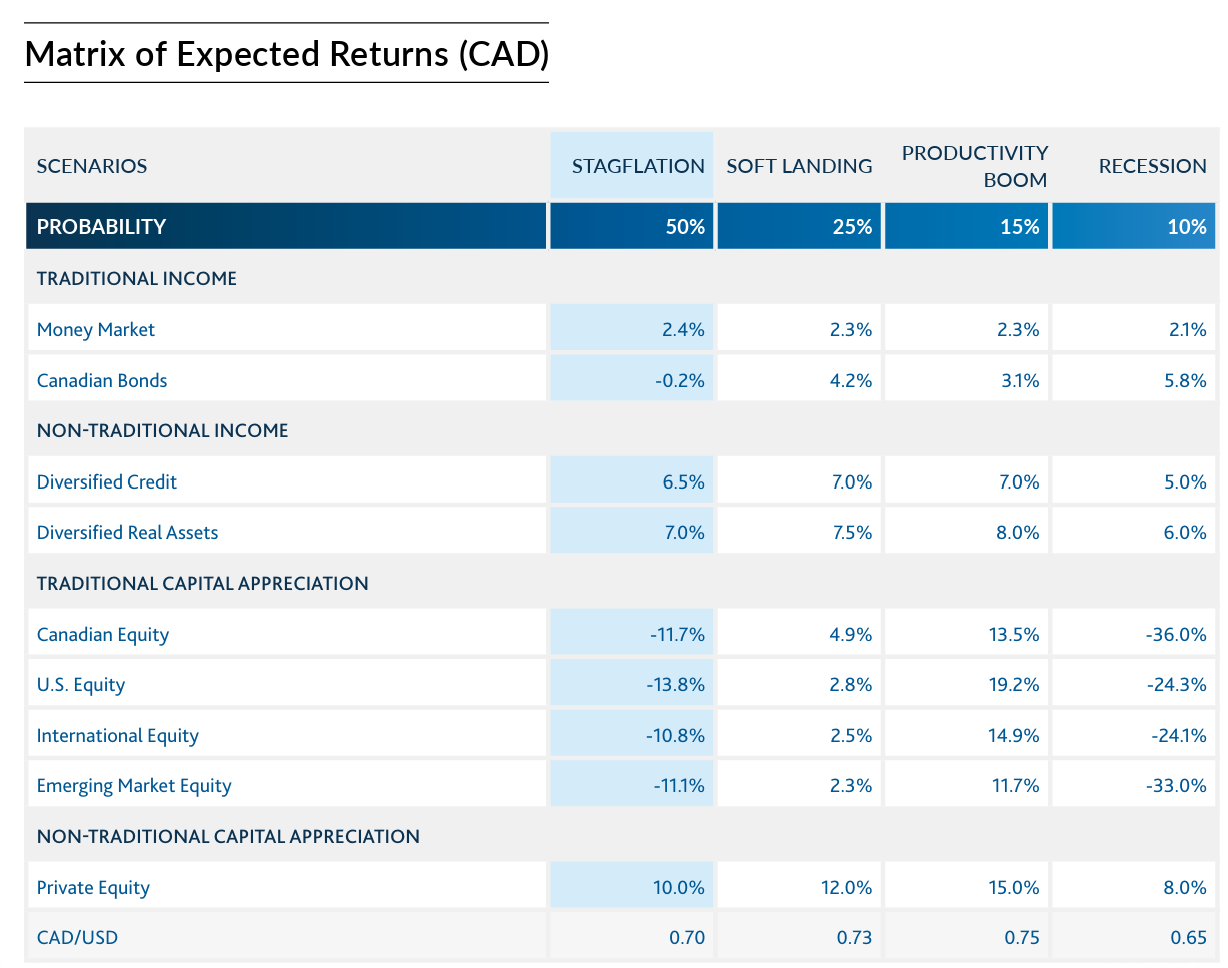

And while these private funds increasingly show signs of cracking and buckling under a complete lack of liquidity, the salespeople do their best to keep the cash pouring in from new investors. Coincidentally, this week I happened to come across this slide from a Canadian institutional money manager’s marketing deck, outlining their expected returns under various economic scenarios.

I’m at a bit of a loss for words here, but here is one that comes to mind: bullshit.

The manager expects that in a stagflationary or recessionary economy, public market equities will get crushed. But private equity, and “non-traditional” income (private debt) will somehow, magically, do just fine.

Now, I just gave you examples of private debt funds around the world imploding, all while global stock markets are clinging near all-time highs. If the stock market falls 10-30%, as the manager believes will happen in these potential scenarios, there is no plausible scenario where these private assets go UP. None.

This goes beyond bad investing, or poor investor education. It’s misleading marketing. Less charitably, it’s a fucking lie.

Earlier this week, a young finance student reached out to me and asked if the story I told in my book about Ted was still how things were done. The idealistic student asked if advisors had become more transparent and honest with their clients. Sadly, I had to tell her that, if anything, things had gotten worse. And they will continue to get worse until yet another generation learns the lessons of the past.

It’s why I write this newsletter. It’s why I wrote this book. Help spread the word. Hit the like button below. Review the book on Amazon. Thanks for reading and thanks for your support!