We're almost there...

The disconnect between public and private valuations is not sustainable

“We know they are lying, they know they are lying, they know we know they are lying, we know they know we know they are lying, but they are still lying.”

— Aleksandr Solzhenitsyn

If you are 30 minutes into an 11 hour drive and the kids ask “are we almost there?” the correct answer is yes.

Parents quickly learn that the truth does nobody any good. And we can comfort ourselves with the idea that the truthfulness of this statement really depends on your definition of the word “almost,” doesn’t it?

And so it is in the world of private assets, as investors (the limited partners, or LPs) depend on fund managers (the general partners, or GPs), to tell them the value of their investments. Like the kids in the backseat, many industry participants believe that LPs are better off not knowing the truth (including some LPs themselves!)

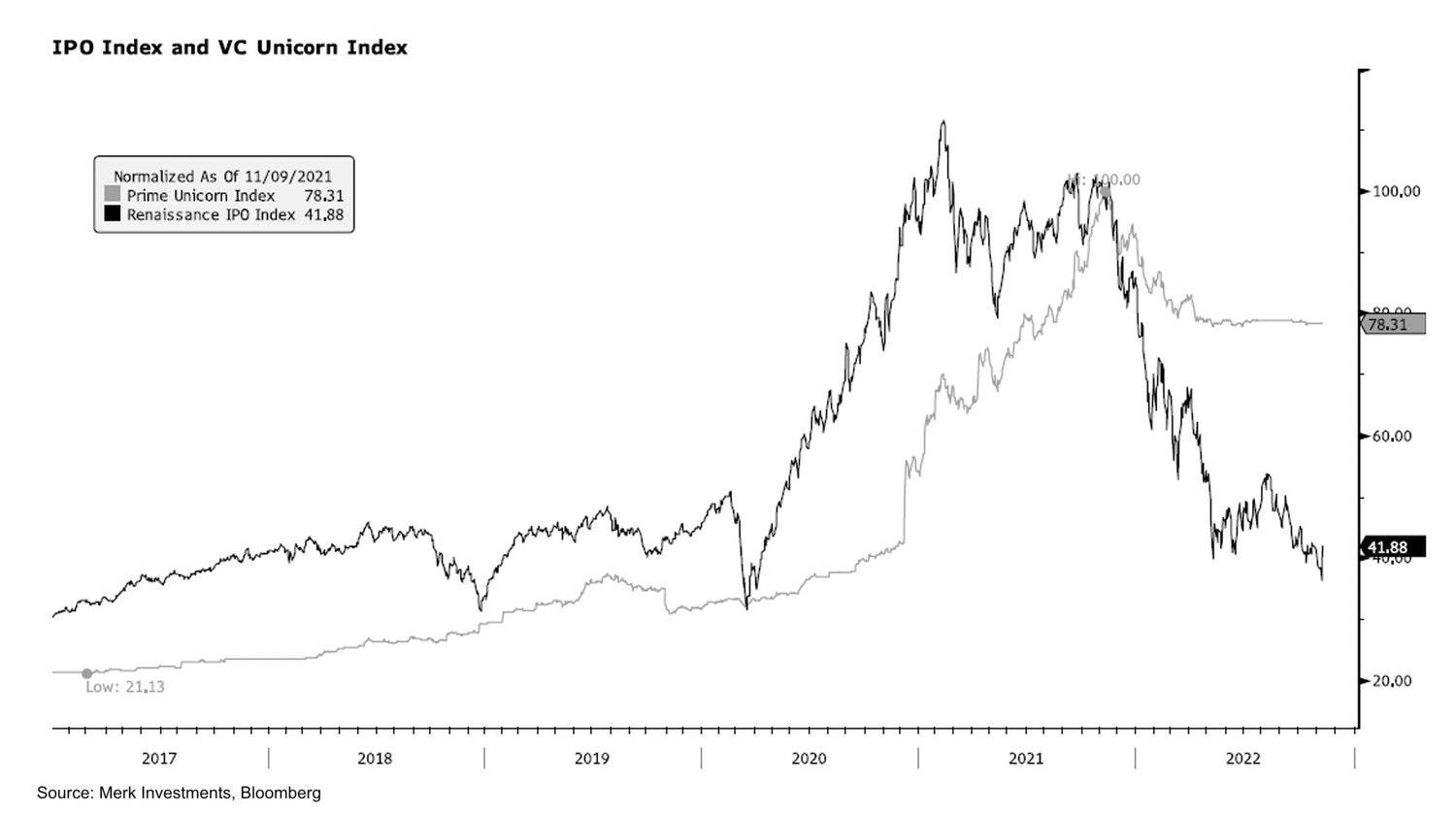

And so you get something like this, and everyone involved pretending it’s the truth:

The Financial Times recently wrote about the “volatility laundering, return manipulation, and ‘phony happiness’ of private equity” and highlighted a theory that the manipulation of values and returns benefits not only investment managers, but their investors as well. While the performance numbers reported may not be accurate, they serve a purpose - to make investment results appear more stable than they actually are.

The idea underlying all of this is that the illiquidity - the inability to sell an investment - is a feature, not a bug, and that some investors are willing to pay up for that “benefit.”

This is the idea expressed by Cliff Asness in his memo titled “The Illiquidity Discount.” You see, traditionally, a major case for adding illiquid investments to your portfolio is that you earn a “premium” for holding assets that don’t have an active market to sell into. If you’re in the institutional or family office world you have heard this argument from every private fund you have evaluated. It’s in all the finance textbooks as well so it’s hard to argue with. But as Mr. Asness writes, “it’s entirely possible that investors are accepting a discounted expected net return for the privilege of not being told the prices.”

The main idea is that all of this obfuscation might keep the kids quiet in the backseat (for a while, at least).

But as Howard Marks writes in a recent memo, the longer the value of public and private assets diverges, the harder it will be to maintain the lie:

As with most things, any inaccuracy in reporting will eventually come to light. Eventually, private debt will mature, and private equity holdings will have to be sold. If the returns being reported this year understate the real declines in value, performance from here on out will likely look surprisingly poor. And I’m sure this will lead plenty of academics (and maybe a few regulators) to question whether the pricing of private investments in 2022 was too high. We’ll see.

My opinion is that this is all fine for investors who understand what they are getting themselves into. I don’t intend to discredit all private investment managers due to the difficulty of valuing their assets. After all, I have made the argument that public market values are full of noise and volatility that don’t do a good job of representing the true value of the assets you own. My issue is with the marketing of these investments, which too often brags about “low volatility” and “uncorrelated returns,” and it’s simply not true.

Investors, including investment committees and beneficiaries, should demand transparency.

As I wrote in Low Risk Rules:

Now ask yourself this question: Would you ever tolerate such obfuscation in your own business? Would you have survived over the years if you did? Would you allow your man- agers to fudge results and hide “temporary” impairments from you on the basis that they were short term in nature?

Of course not.

Now why do you allow it in your investment portfolio?

If you recall those days sitting in the backseat, wondering when the interminable car ride would finally be over, you know that Mom and Dad knew you were in for several more hours of pain, but didn’t dare to tell you. Sometimes the lie is a small price to pay to keep you quiet and compliant. But the truth comes out eventually… and we are almost there.

A note to end 2022

On a personal note, the past few years have been a rollercoaster. Seeing my book in print was a highlight, but that was just the beginning. Thanks to the book and the writing I’ve begun to do online I’ve met a ton of awesome people and had the opportunity to reconnect with old industry friends from years past. It’s been an amazing experience.

Thank you for your support, and for taking the time to read my ramblings and come along for the ride.

Merry Christmas, gang. I wish you peace, contentment, and prosperity in 2023.