Timing is everything

Definitely early. Probably not wrong.

When I started working on Low Risk Rules in mid-2020, the markets were in a weird place. A stimulus-driven recovery had taken hold, but nobody believed it was real. A bunch of bored people sitting at home with nothing to spend money on decided to start gambling. Whether it was Zoom and Peloton, Bitcoin, or the meme stock of the day, gambling became all the rage.

I knew the market speculation wouldn’t end well. With a publishing date target of June 2022, I feared that the speculative fervour would collapse under its own weight long before the book’s release date, making it as relevant as last week’s newspaper.

But surprisingly, the timing worked impeccably. The market rose throughout 2021, before reversing course just as the calendar ticked ‘22. In mid-2022, we were in the midst of what I believed would be a long overdue unwind of the excesses of the last decade, particularly in tech-land, where a group known as the “Magnificent Seven” were leading us to profits and glory.

Of course, nothing ever works out as you think it will. Near the end of 2022, ChatGPT was released to the public, creating an AI investment frenzy that carries the market to this very day.

Without the massive investment in the data centers and technology required to support our AI-centric future, many believe we would be in a recession today. Is it just putting off the inevitable reckoning?

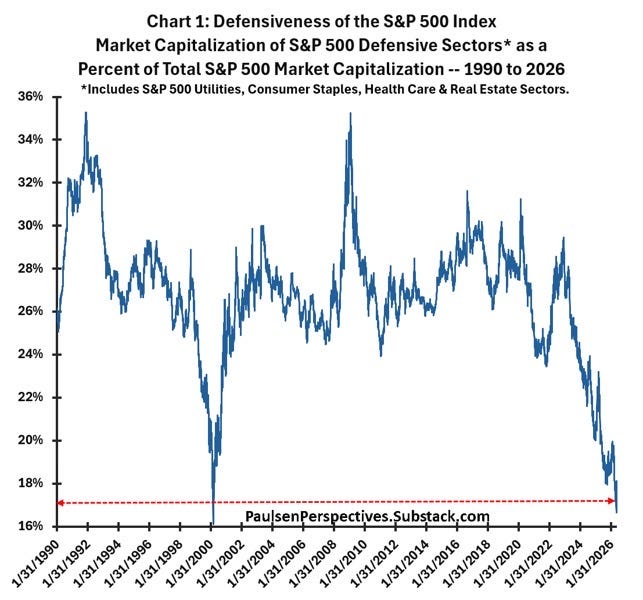

Investment dollars have fled the “old economy,” or any sectors that might be disrupted by the next iteration of Claude or ChatGPT. Conservative, low-risk investing (the kind I wrote about for 280 pages) is going through one of the worst extended relative performance periods in my lifetime. Maybe it turns out that my timing wasn’t so great…

As a rough illustration, here’s a chart courtesy Jim Paulsen that illustrates the underperformance of defensive stocks in dramatic fashion. Yes, last time we were here was at the market extremes of 2000.

But this time is different, right?

Also this week, CNBC broadcast an incredible guest spot by fund manager Jeremy Grantham. Grantham is making a media push, also appearing on the Diary of a CEO podcast, and I just want to make the disclaimer that I actually don’t agree with a lot of his current opinions, so don’t consider this a blanket endorsement. But one thing he has done reliably over time is root his forecasts in observable, measurable data. If you’re interested, his firm GMO regularly forecasts asset class returns based on current valuations, which at least proves his “value” bona fides (personally, I find this forecasting exercise marginally interesting but mostly useless).

And then there’s Joe Kernan, who has been a CNBC anchor as long as I’ve been aware. Joe made it known in no uncertain terms how he feels about Grantham, his methods, and his skepticism about the current speculation in stocks and cryptocurrency.

Watching this, I felt like it was the kind of exchange that we would remember years from now. Not just because it was so abrasive, but also because the old-school value-based fund manager was being schooled by the TV anchor who’s only argument was “price go up.”

This is me reading the tea leaves, looking for warning signs, and starting to think about how vulnerable a market is where the gambling instinct takes over, and where we openly ridicule the people who dare to question the bullish narrative.

For what it’s worth, here are a few choice Buffett headlines from 1999 (via Thierry):

I don’t know if this is the top. But I do know that this is what tops look like.