The only thing we know for sure...

Is expecting a return to normal a losing bet?

Over the weekend I was talking to a young aspiring homeowner who was glad to see housing prices finally coming back down to earth. His only complaint was that the decline in home prices was not yet reflected in more affordable mortgage payments, due to the dramatic rise in interest rates.

“I’ll just wait for rates to get back to normal.”

This echoes what I’ve heard from so many people over the course of the last year. Perhaps this is a consequence of listening to central bankers and politicians who assured us that any inflation we experienced would be “transitory.” Or maybe it’s just plain old recency bias.

Here’s the thing: there is no guarantee that either inflation or interest rates will come down, and if they do, you can’t be sure that any dip won’t be temporary.

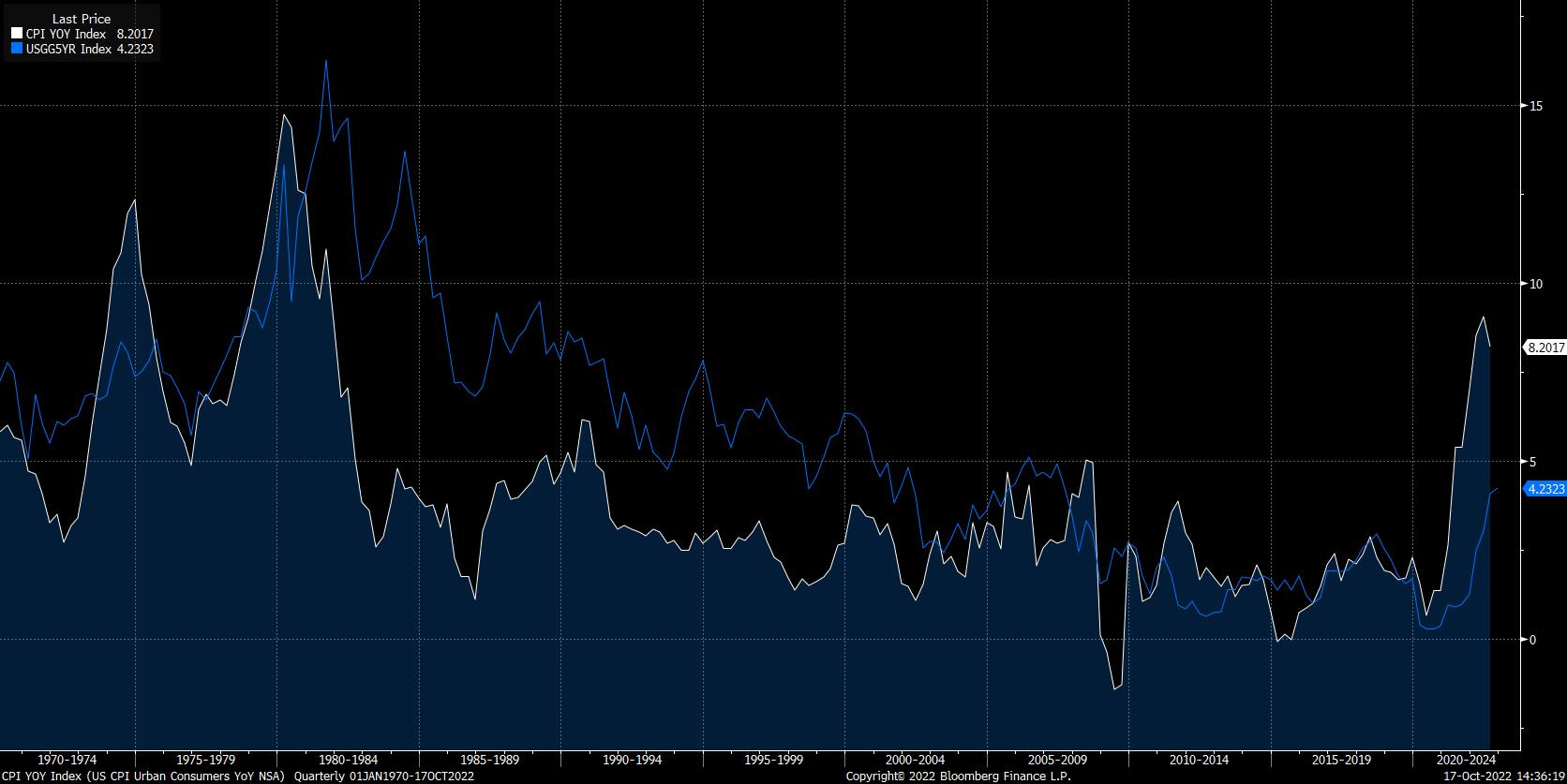

The chart below shows the path of inflation and interest rates (reflected by the 5-year US Treasury bond) going back to 1970. You’ll see over on the left side of the chart that inflation spiked twice (as shown by the white line), and that it took a final, significant surge in interest rates (that’s the blue line) in the early 1980s to finally get prices under control.

Compare this to where we are today, at the far right of the chart. There’s no reason that what we saw in the 1970s can’t occur again. If it does, we are only at the very beginning of our fight against inflation. This means that rates can go significantly higher from here.

There are those who believe that it is necessary to take interest rates above the rate of inflation to finally bring prices under control, and if you note that the 5-year government bond rate is still far below the reported inflation rate, this should be very concerning!

Now I’m not saying that this is what’s going to happen. I am the first to admit that I have no idea where we go from here. All I’m saying is that this could happen, and I wouldn’t want to construct an investment strategy around the idea that we will soon revert to “normal.”

As we’ve seen post-pandemic, the idea of “normal” is forever evolving. Occasional seismic shifts serve to shake us out of our view of how the world should be. Perhaps we are seeing such a shift in the interest rate market right now.

Now, more than ever, I want to stress the importance of staying nimble and liquid. This is not the time to commit large portions of your portfolio to illiquid investments or aggressive strategies.

…nobody knows anything

In the depths of the market collapse of 2020, I heard a throwaway comment on a podcast that stuck with me. One of the hosts was speculating on where we might find a bottom for stocks, and what the eventual recovery might look like.

“The only thing we know for sure,” he said, “is that we won’t be hitting new highs again this year.”

That wasn’t a controversial statement. There was probably not an investor alive at the time who would have disagreed with it.

And so it was, that mere months later, after a rally that defied all expectations, the S&P 500 hit a new high for the year.

The only thing we know for sure… is that nobody knows anything.