Checklist Series, Part 13: Fortress Incorporated

Only the strong survive

If we are building a low-risk equity portfolio, we need to start with a solid foundation. And that foundation is the financial position of every company we invest in. This begins with a solid balance sheet. What they call “fortress financial statements.” We want to know that the next time the world crumbles around us, we don’t have to worry about the survival of companies we own.

Ideally, we want to see net cash on the balance sheet. If there’s debt, I want to know that it’s well covered by operating cash flow, even in the most dire of circumstances. If I can be sure that the company I own will not be forced to restructure in order to pay its debts, then I shouldn’t care too much about what the stock price is doing, even when it’s crashing through the floor.

Numbers matter (and they also sometimes lie)

Understand the various debt ratios. Make sure that interest costs are covered by cash flow. Ensure that the company has adequate short-term working capital.

If there’s debt outstanding, put it under the microscope. Is it fixed, or variable? What is the maturity schedule? Are there any loan covenants you need to watch out for? Are there any off-balance sheet liabilities or other commitments?

This is a timely topic right now. The AI data center buildout is sucking up record amounts of capital. But these big hyperscalers want to maintain their strong balance sheets and investment-grade ratings. So they have been using off-balance sheet vehicles to finance the buildouts. Understand these arrangements. Don’t take debt ratios at face value.

Leverage can turn a low-risk business into a high-risk equity

Remember: the value of a company’s equity is a residual. It’s the excess value of the business over other fixed obligations. Imagine two identical companies: one with high debt, and one with no debt. The one with debt financing will provide equity investors with higher returns on the way up… but could ruin them on the way down.

Too much debt can turn a low-risk business into a high-risk equity investment. Too much debt financing that comes due at the wrong time could ruin a company. Woe to anyone that had significant bonds maturing in the financial crisis of ‘08/09. Back then, it turned reliable, stodgy businesses like Diageo into volatile stocks as investors worried about refinancing risk.

And so, I have learned through experience and over time, not to ignore the balance sheet, no matter how good things appear to be. Tides inevitably turn, and you don’t want to be caught relying on debt markets when liquidity dries up.

Yes, that means less juice to a stock price on the way up. That’s a compromise I’m willing to make in exchange for peace of mind when others are panicking.

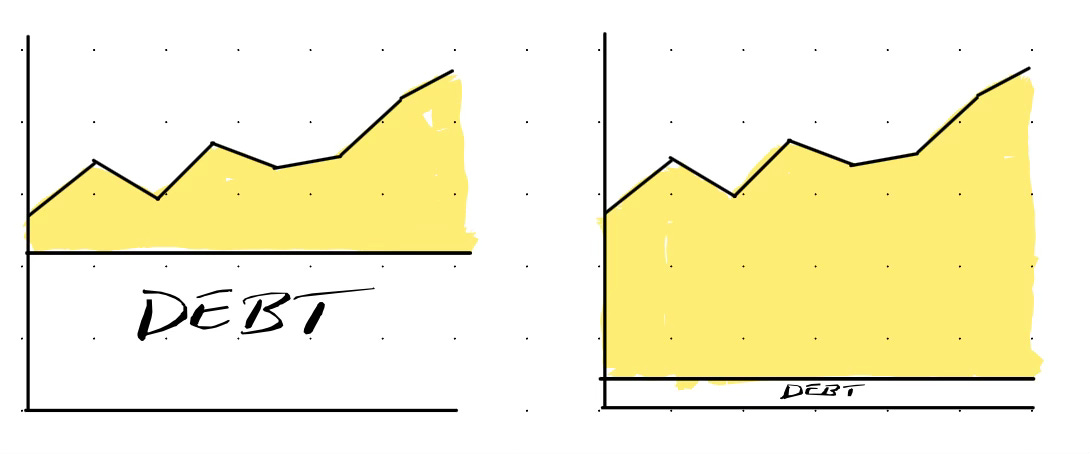

Too much torque

Here are two rough illustrations of a company’s enterprise value over time. The one on the left has a high level of debt (the unshaded portion at the bottom). The company on the right has a lower level of debt.

As you can see from the shaded segment, equity holders of the more leveraged company experience a higher percentage gain as the company’s value goes up. That’s good, right?

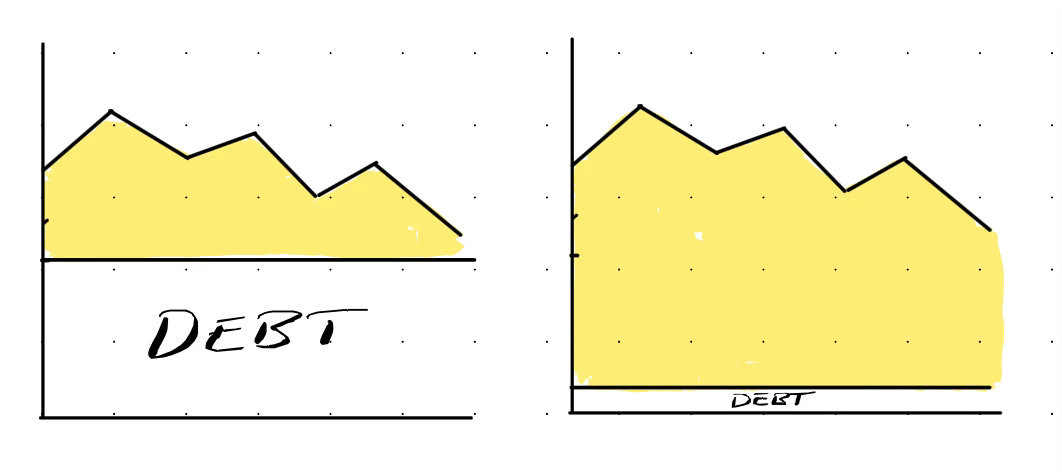

Maybe! Let’s see what happens if the company’s enterprise value goes down:

Oh, snap! The equity holders in the more highly leveraged company are almost wiped out, while the shareholders of the company with less debt still own the majority of the value of the business.

It’s actually that simple: a more conservative balance sheet means an enhanced ability to survive business slowdowns and recessions. It means more time for a management team to pivot from a strategy that isn’t working.

Not all stocks are created equal. Want to manage risk in your portfolio? Start by avoiding stocks that can get into trouble from carrying too much debt. It’s a bit of common sense advice that is too often forgotten when the party is in full swing.